Why Use Nielsen Valuation Group for Business Appraisals?

Nielsen Valuation Group provides unbiased business valuations in full compliance with IRS Revenue Ruling 59-69.

Our appraisals are designed to determine the fair market value of the business, taking into account the track record and current situation in the company, while avoiding speculation.

We are completely independent and have no other interest than to provide you with a well-balanced and nuanced valuation. Our assessments are robust and can withstand the rigorous scrutiny of negotiations or litigation.

The facts on the ground, as opposed to hypothetical assumptions, are at the heart of every valuation.

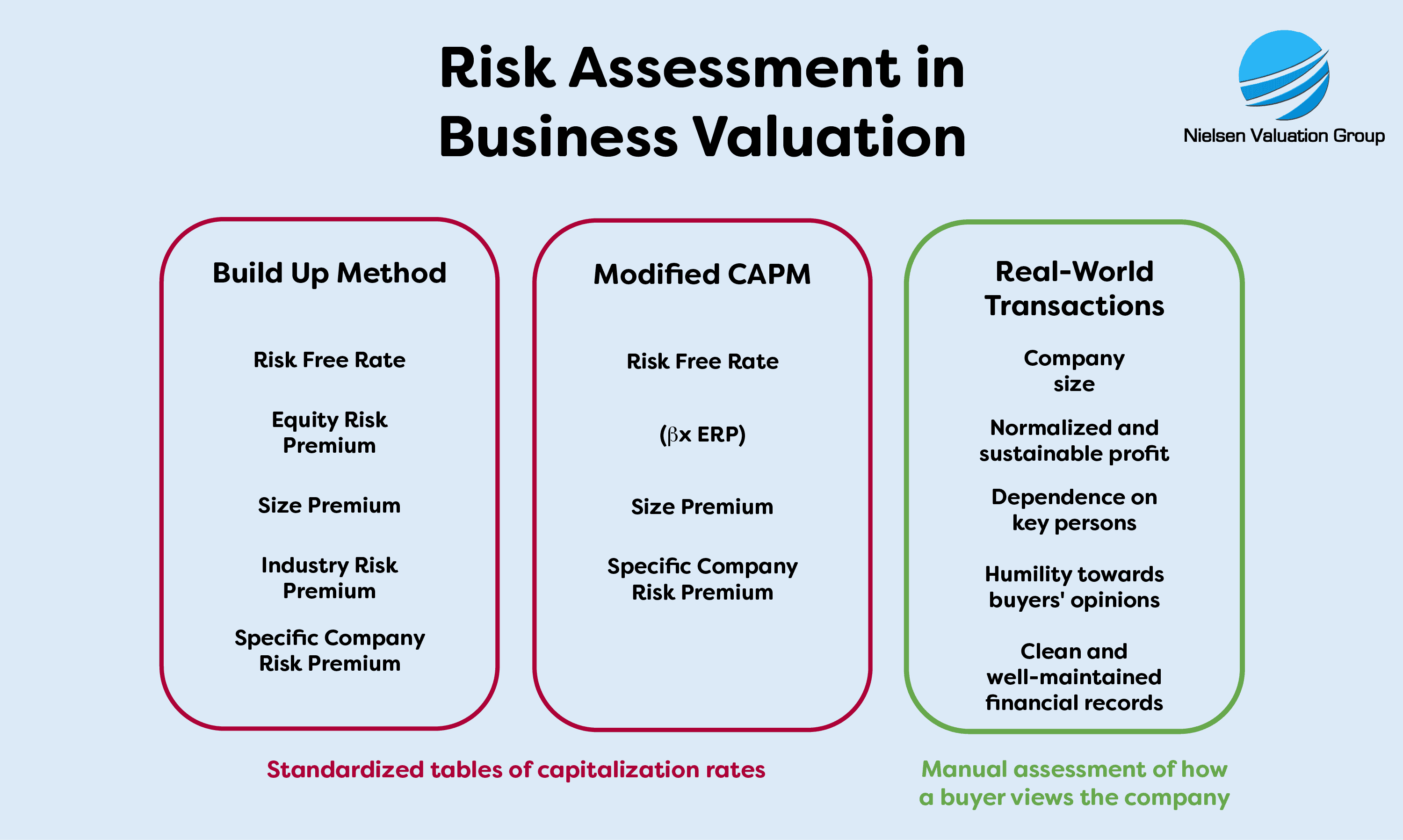

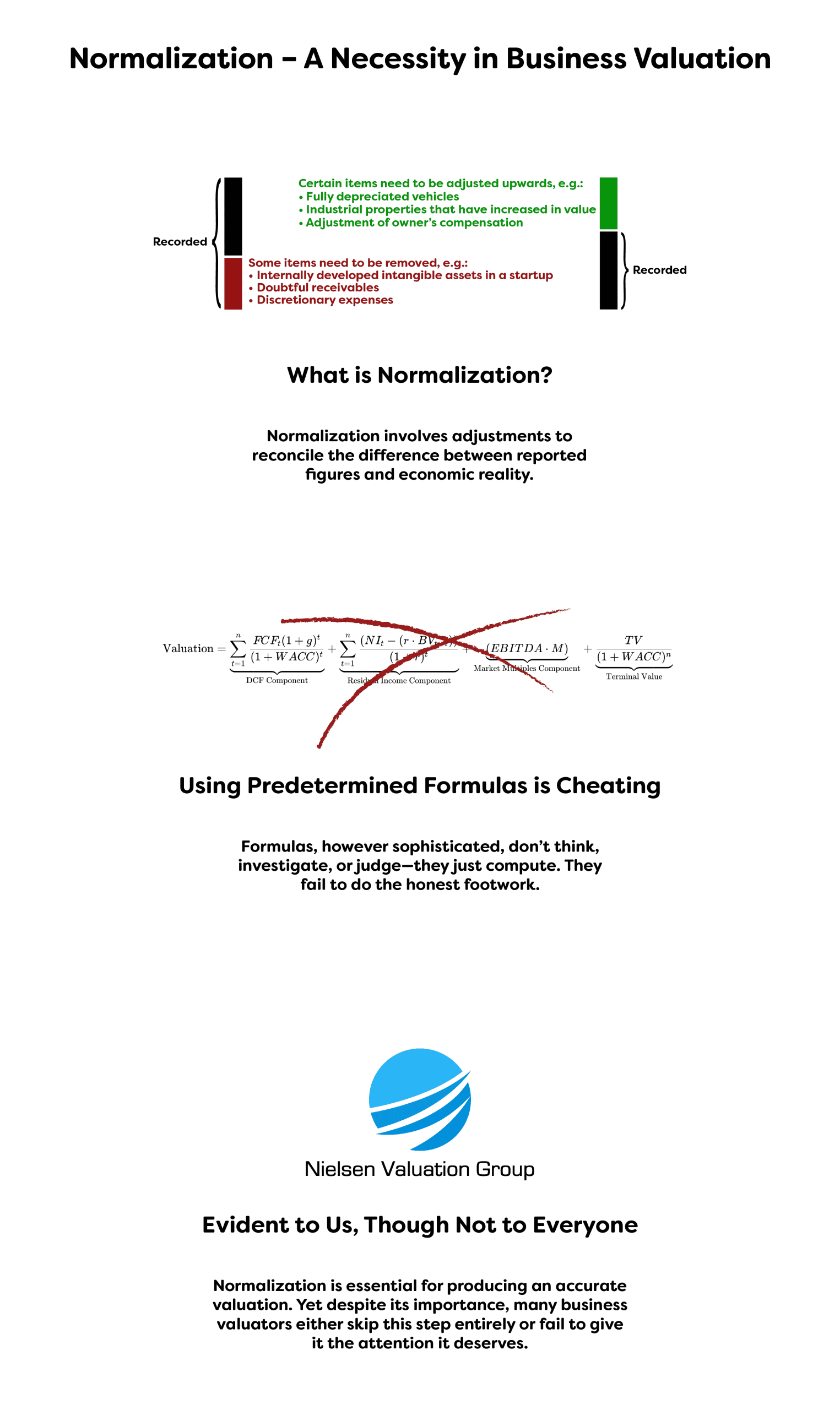

We always begin by normalizing the income statements to remove irregularities, unrepresentative expenses, one-time payments, and similar. We also normalize the balance sheet to reflect market value of assets and adjust liabilities when needed.

If necessary, we apply a valuation discount for lack of marketability, lack of control, or key person discount. We do the calculations ourselves and do not rely on theoretical studies or standardized tables.

The result is a firm valuation to be used in the intended situation and trusted by everybody concerned.

We Are Fully IRS Revenue Ruling 59-60 Compliant

As mentioned above, we fully comply with the Internal Revenue Service (IRS) Revenue Ruling 59-60, which is surprisingly rare among business valuators.

Following this ruling means that we place great emphasis on the practical aspects of real world transactions. Equally, or more so, than what is required by associations and certifications such as the National Association of Certified Valuators and Analysts (NACVA), the American Society of Appraisers (ASA), or the American Institute of Certified Public Accountants (AICPA).

Our appraisals prioritize aspects that determine actual transaction outcomes, as opposed to theoretical assumptions about future potential. We thereby bridge the gap between real-world decision making and standardized methodologies.

The following sections describe how we do this in practice.

We Never Rely on Standardized Capitalization Rate Tables

Many business valuation firms use standardized tables of capitalization rates for convenience. Such tables show cap rates based on, for example, industry type, business size and stability, growth rate assumptions, and the like.

We don’t.

IRS RR 59-60 states:

”No standard tables of capitalization rates applicable to closely held corporations can be formulated.”

Instead, we make an in-depth assessment of the business, what risks are involved, its stability or irregularity of earnings, among other things.

We Never Use Predefined Formulas

Similarly, many business valuation companies use a predefined business valuation formula to arrive at a price. This allows them to save time, while the complex calculations give the impression of being precise.

They give a false sense of security that the valuator knows what he or she is doing, while the estimated value can be completely wrong.

It is a frightening fact that some of the business evaluations out there rely solely on formulas based on unadjusted balance sheet and income statement numbers.

Such calculations are a waste of money.

Again, the IRS is very clear:

“No general formula may be given that is applicable to the many different valuation situations arising in the valuation”

“Valuations cannot be made on the basis of a prescribed formula.”

“Such a process excludes active consideration of other pertinent factors, and the end result cannot be supported by a realistic application of the significant facts in the case except by mere chance.”

When you hire us for a private company valuation, we will perform a detailed evaluation of the business in question, rather than using formulas. We will take a close look at its financial and operational history, current condition, and future prospects. If required, we will conduct on-site inspections and interviews.

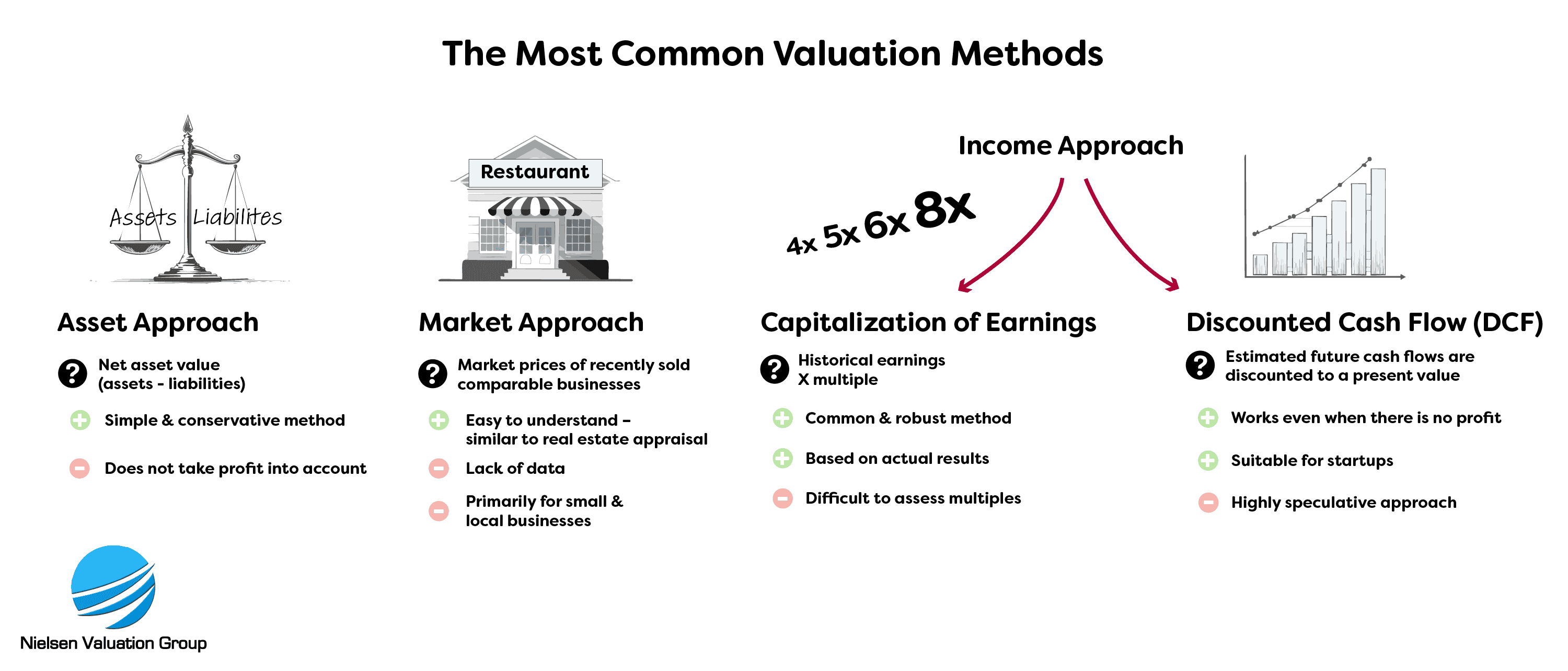

The Most Common Business Valuation Methods

When you engage Nielsen Valuation Group, we use one or more business valuation methods. Knowing which method to choose and how to apply it in practice, without relying on pre-determined formulas, is key to determining the fair market value of the business.

There are three business valuation approaches:

- Market Approach

- Income Approach

- Asset Approach

We may use more than one approach, as this often strengthens the valuation, depending on the situation. We always consider the type, size and complexity of the business, as well as the purpose of the valuation, when deciding which approach to use.

In the following paragraphs, we will introduce you to these three valuation approaches.

Market Approach

The market approach is based on the selling prices of other similar businesses.

It is a powerful valuation approach because real transactions give a good indication of what the business is worth in the market.

However, this approach often suffers from a lack of data, and the problem is twofold. First, there is rarely enough sales data to make a meaningful and reliable comparison. Second, the data sets that are available often suffer from unverifiable or unreliable data.

In most cases, the market approach can be applied to local businesses such as restaurants, supermarkets, or coffee shops. If used, the available data must first be carefully scrutinized and cleaned of statistical outliers.

It is best used in conjunction with the income approach or the asset approach.

Read more about the market approach

Income Approach

The income approach is based on the earnings or cash flows of the business. It looks at past performance and current risk to arrive at an estimate of the value of the business.

A company’s ability to generate earnings is a critical factor in most company valuations.

There are several valuation methods within this approach. The two most commonly used are

- Discounted Cash Flow (DCF)

- Capitalization of Earnings

Read more about the income approach

Asset Approach

The asset approach seeks to determine the net asset value of the business. To reflect the fair market value of the business under this approach, it is necessary to consider the market value of the assets and liabilities, not just the book value.

This approach is often used for business with lots of assets and businesses in liquidation.

It does not take earnings into account, which is why it is preferable to combine it with the income approach in order to obtain a valuation that reflects a realistic market price.

Read more about the asset approach

Weighting and Combination of Valuation Methods

When performing a business valuation, it is common to combine or weight methods. These two options sound similar, but there is a big difference:

- Combining is typically done by adding the net asset value from an asset approach valuation to an income approach valuation.

- Weighting means that each approach represents a certain percentage of the valuation. For example, 70% of the valuation might be based on the income approach and 30% on the asset approach.

Weighting is surprisingly common among business valuation advisors. However, what may seem innocuous at first glance has far-reaching implications when examined in detail.

Example 1 – When weighting is done incorrectly

Example 2 – How predetermined formulas make it even worse

There is no logic in weighting the actual market value of the asset by a certain percentage. It always means that assets will be undervalued. This may be compensated for by an overvaluation of earnings. But what is the point? And why use such arbitrary weights?

The IRS is clear on this point as well:

“Because valuations cannot be made on the basis of a prescribed formula, there is no means whereby the various applicable factors in a particular case can be assigned mathematical weights in deriving the fair market value. For this reason, no useful purpose is served by taking an average of several factors.“

We carefully consider all relevant facts, as outlined in RR59-60 and manually determine their significance. Many times, this leads to a combination of valuation methods, to even out the differences that otherwise occur. This may in some cases lead to adding the normalized net asset value to an income approach valuation.

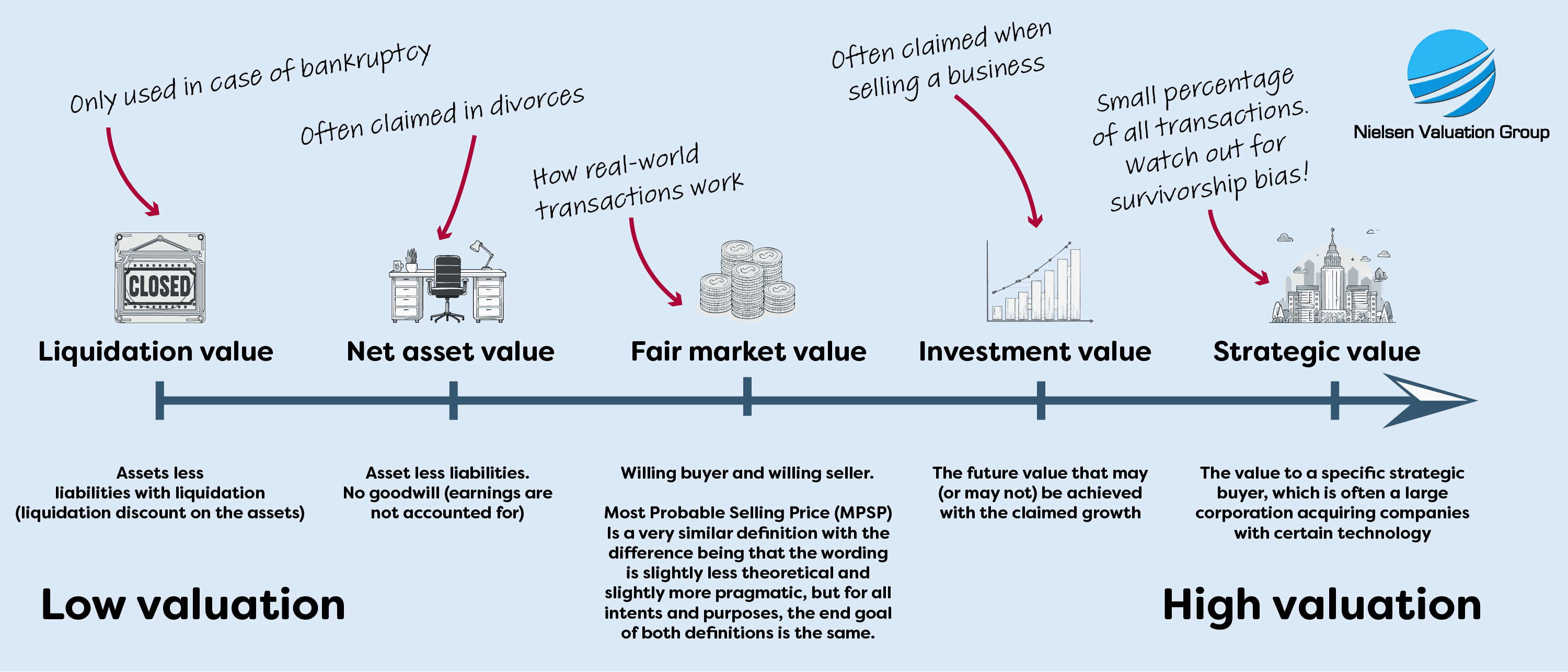

How Much Is My Business Worth?

Are you thinking of selling your business? If so, you should focus on determining its fair market value. At this price you are likely to find a buyer.

The IRS defines it as:

“Define fair market value, in effect, as the price at which the property would change hands between a willing buyer and a willing seller when the former is not under any compulsion to buy and the latter is not under any compulsion to sell, both parties having reasonable knowledge of relevant facts. Court decisions frequently state in addition that the hypothetical buyer and seller are assumed to be able, as well as willing, to trade and to be well informed”

If you simply apply a standardized formula, you will not uncover fair market value. For example, if you pick a multiple from a standardized cap rate table and arbitrarily apply it to five or ten year earnings averages, the value may or may not be what a buyer is willing to pay.

This is what the IRS says:

“Prior earnings records usually are the most reliable guide as to the future expectancy, but resort to arbitrary five-or-ten-year averages without regard to current trends or future prospects will not produce a realistic valuation.”

In other words, past performance is a reliable guide to current value, but it must be evaluated manually, not by a prescribed formula or standardized approach.

Two Mistakes Business Sellers Often Make

We see two common misconceptions among business sellers. Understanding these two issues will increase your chances of finding a willing buyer.

Mistake One: Survivorship Bias

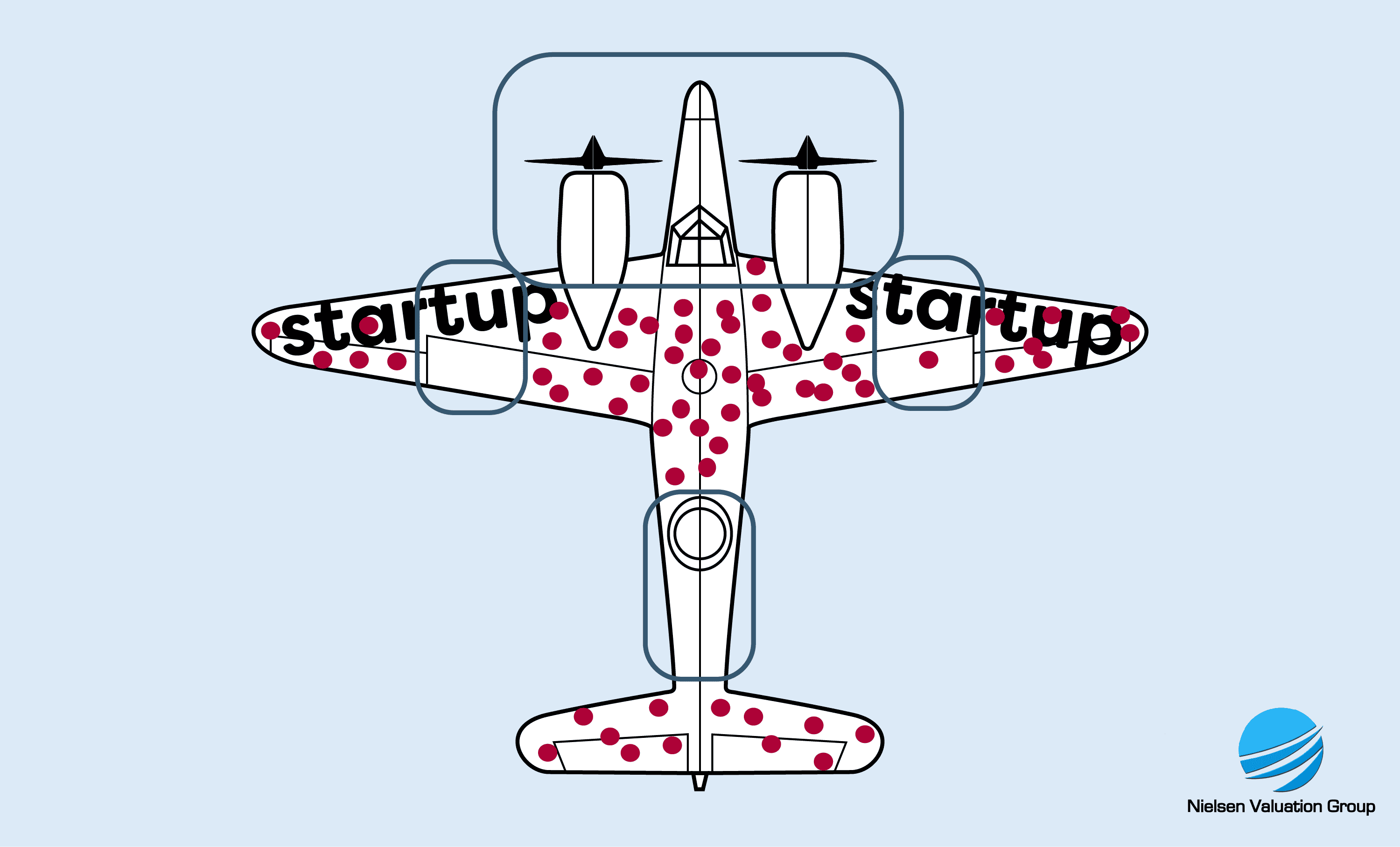

This first mistake is common among entrepreneurs and small business owners, especially startups. They often have a survivorship bias when assessing the value of their business.

They point to highly successful startup cases like Uber, Meta, Alphabet or Telsa and say things like:

- “That’s where we’re going!”

- “Look at them – we are doing the same thing, but in our industry. We deserve a similar valuation.”

If you turn to the buyers, you will understand that it is not that simple. Buyers and investors know that only around 10% of startup companies survive in the long run. If these investors want to survive in the long run, they have to be smart about how they allocate their money. As a result, what they are willing to pay is often significantly less than what startup owners typically hope for.

The term survivorship bias comes from World War II. As fighter planes returned to base, they were analyzed to determine where they should be reinforced. It was noted where they had been hit, and analysts saw that the cockpit and engines seemed undamaged by the shelling. The conclusion was that these areas did not need additional armor. However, the conclusion was wrong because it was based on survivors. The reality was that planes hit in those areas never made it back to base.

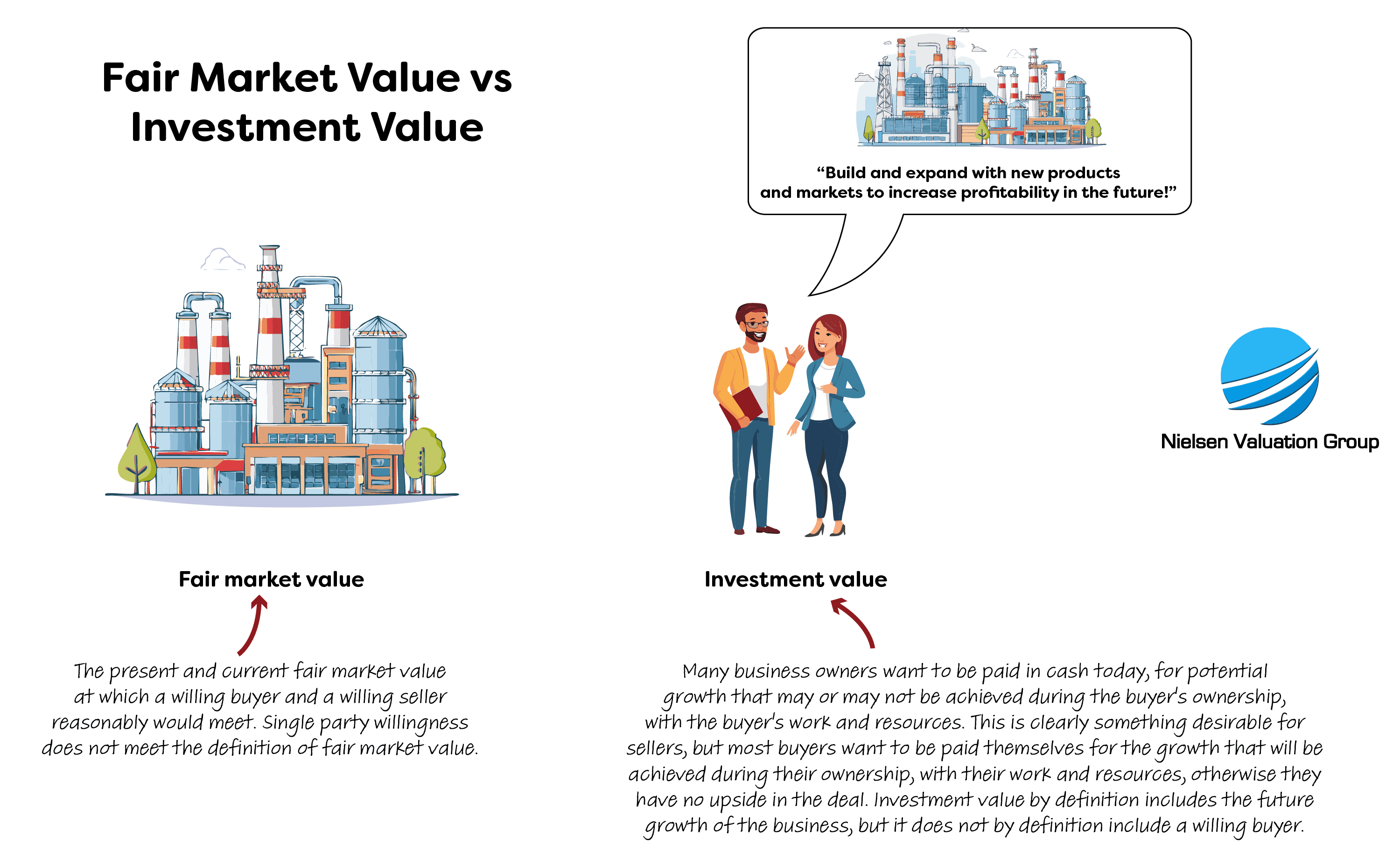

Second mistake: Not understanding fair market value

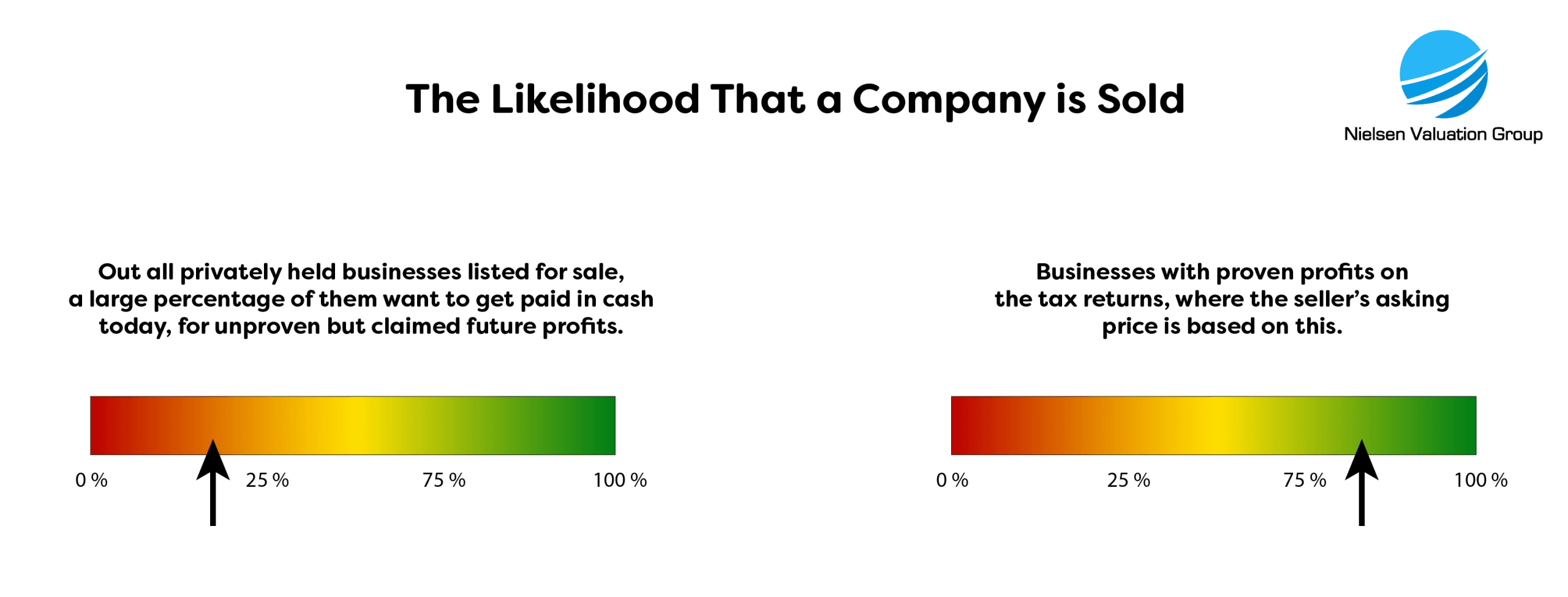

There is sometimes great confusion among sellers about the difference between fair market value and investment value.

Many business owners would like to be paid upfront for the future potential in their business. They can point to various highly lucrative aspects of the business that “just haven’t been realized yet, but are very likely to happen”.

However, a buyer will almost never pay for such potential. Whatever potential exists is seen as the upside of the investment, a reward for the risk the buyer is taking by investing.

Buyers want to pay the fair market value of the business – what it is worth here and now in a free and open market. What the seller dreams of is called the investment value, which is what the buyer hopes to achieve after the purchase.

If you are a seller and expect to be paid for potential, you can only expect to be paid with potential. For example, in shares of another high-risk company.

Don’t Pay for a Yacht When You’re Buying a Raft

Some sellers and brokers try to justify higher prices by pointing to what a business could become — not what it actually is. They focus on potential growth, imagined improvements, or hypothetical success stories that haven’t materialized. But pricing should reflect the business as it stands today, not a version of it that doesn’t yet exist.

It’s like trying to sell a basic inflatable raft at yacht prices because someone could one day add an engine, radar, and luxury seating. A reasonable buyer wouldn’t pay yacht prices for that raft, no matter how ambitious the plans. The value lies in what’s being delivered now — not in what someone else might someday build.

Price What Exists — Not What’s Imagined

A credible valuation considers the full picture: current assets, earnings, risks, and operations — all in the context of what has actually been achieved. While the future matters, it’s just one factor among many. The totality of the circumstances — not just optimistic projections — determines value. Just like boats, businesses should be appraised based on their present condition. Just like it is incorrect to price a raft like a yacht, it is equally incorrect to price a new yacht, like an worn out one, just because the projections are that the new one will be worn out too one day.

Common Business Appraisal Mistakes

- Wrong approach: If you value a fast-growing service business with substantial revenues but few assets using only the asset approach, the result will be completely misleading. Similarly, if you value a distressed business in liquidation using the income approach, the valuation will be useless.

- Skip normalization: A surprisingly common mistake, even among experts. It means taking the face value of the balance sheet and income statements, instead of evaluating and adjusting the numbers in detail.

- Incorrect weighting of earnings: Theoretical valuations ignore earnings volatility. Formulas that follow industry averages will lead to erroneous conclusions, especially in the valuation of a small business, where fluctuations can be large.

- Failure to understand the business: Many business appraisers never look beyond the numbers, but financial statements can be manipulated. To do a thorough valuation, it is necessary to consider the nature of the business, its current situation, where it came from, where it is going, its people, its leaders and its culture.

- Use an online business valuation calculator: All business valuation calculators, whether free or paid, use pre-determined formulas and therefore do not take into account the specifics of the business. They also do not use normalized figures from the balance sheet and income statements, which leads to additional miscalculations.

- A valuation is always accurate: If you were to hire five different appraisers for an enterprise valuation, you would likely get five different estimates, possibly with a wide variance between them. All valuations are approximations, and some are more speculative than others. The real price is what somebody is willing to pay for the business.

- Have too much faith in your business broker: They may have good contacts in the local market, but they often still fail to sell your business. Why? Because the incentives are wrong. They often overvalue the company to get a higher commission. Unfortunately, this results in a large percentage of businesses remaining unsold.

Let Us Help You with Your Business Valuation

Nielsen Valuation Group delivers unbiased, IRS RR 59-60 compliant business valuations across the United States, grounded in real-world transactions. Contact us today for a free 30-minute consultation.

Want to go with a cheaper option or even do the valuation yourself?

Nothing is stopping you, but...

You may lose the lawsuit, due to the valuation failing to be waterproof.

You may never settle the conflict, hurting the relationship with your counterpart.