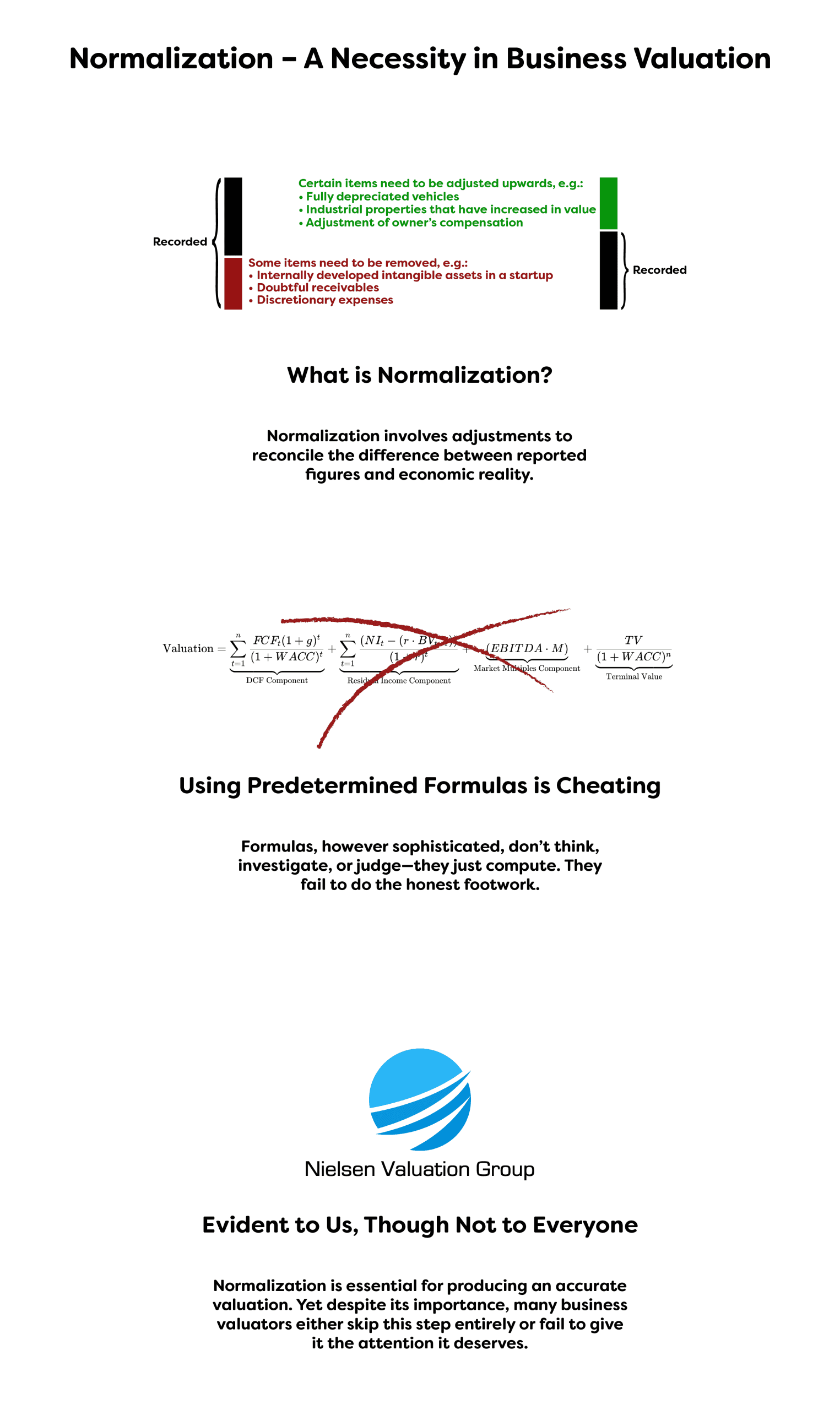

Engagement Is the Best Indicator of Valuation Quality

A lot of five-figure business valuations are not any better than what ChatGPT can produce with the right instructions, or what you can buy for $250 on Fiverr.

Why?

Because what makes a valuation accurate and useful is not the amount of copy-pasted text, generic charts, or recycled analysis.

What makes a valuation good is how well the valuator gets to know the business—and their experience with real-world transactions.

Many business valuators are known for sticking to heavily standardized methods and often fall short when it comes to acknowledging real-world dynamics—that can require meeting the buyer and seller at the business itself, a few hundred miles away, after business hours.

Since they do not truly get to know the buyer, the seller, or the business beyond surface-level data, their valuations rarely reflect the actual deal.

These so-called “valuations” are often more like market statistics reports than true assessments of individual companies.

While there is little to no correlation between the amount of generic charts, recycled analysis, and boilerplate copy-paste content, there is a real correlation between the level of engagement from the business valuator and the accuracy of the valuation.

Engagement can be defined by whether they sent you a one-size-fits-all form to fill out—or actually engaged in real conversation about what’s relevant in your specific case and requested additional documentation for the parts that will move the needle in your specific valuation.

Relabeling and Misrepresentation

It has become increasingly common to present white label 3rd world country business valuations as if they were American valuations, without any disclosure to the client. If the same misrepresentation were applied to a physical product, it would constitute a violation of country-of-origin labeling laws and the Federal Trade Commission Act, and could fall under general fraud statutes.

This type of misrepresentation is not only unethical, but also easily exposed in court.

While some formalities are required, they matter far less than whether the real legwork has actually been done. And that (the legwork) is precisely what the above mentioned valuations tend to skip and replace with generic charts and recycled analysis dressed up to look credible.

Our valuations are made in the Texas by Christoffer Nielsen, the founder of Nielsen Valuation Group, not by outsourced low-cost labor overseas, or junior assistants or software that overlooks the factors that move the needle.

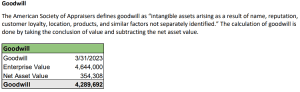

Accountability

How would you feel if your business valuator treated goodwill as a residual figure rather than a reflection of the business’s ability to generate earnings? Several commercially motivated third parties promote their own credentialing standards that rely heavily on standardized table of capitalization rates and predetermined formulas, even to the extent where goodwill becomes a residual number.

As stated in ASA materials:

“The calculation of goodwill is done by taking the conclusion of value and subtracting the net asset value.”

IRS Revenue Ruling 59-60 takes a fundamentally different position:

“In the final analysis, goodwill is based upon earning capacity. The presence of goodwill and its value, therefore, rests upon the excess of net earnings over and above a fair return on net tangible assets.”

This methodology disregards the requirements of Revenue Ruling 59-60 and therefore, by extension, fails to comply with the Internal Revenue Code.

Christoffer Nielsen

Phone: (737) 232-0838

[email protected]

Nielsen Valuation Group LLC

- Number of business valuations completed: 250+

- Number of valuations for disputes/divorces: 70+

- Largest client (revenue): $87 million

- Majority of customers: $2 million to $50 million in revenue

- Largest client (valuation): $155 million

Want to go with a cheaper option or even do the valuation yourself?

Nothing is stopping you, but...

You may lose the lawsuit, due to the valuation failing to be waterproof.

You may never settle the conflict, hurting the relationship with your counterpart.